_

_Viewed 19695 times | words: 7166

Published on 2020-05-05 16:54:53 | words: 7166

Well, just to remove any doubt: yes, the title is a reference to a movie 1976 (worth watching: "Marathon Man").

I was thinking at that movie few days ago, on May 2nd, when I shared a short post on my facebook profile

But yesterday I was thinking about a forty years older movie, that reminds me of some of the delusional technocratic noises that routinely surface in Italy, and that are becoming so common during this pandemic crisis.

Well, anybody and his dog is currently rehashing bits of news, commentary from scientists and assorted specialists (from politics to philosophy to social sciences to anything you can think about).

It feels almost as if many, at least in Italy, were vying for their own "15 minutes à la Andy Warhol".

In Italy, this has an additional value added: there are many potential opportunities to lead one of the routine quangos or commissions that will be set up to think about planning the management of the identification of solutions to be implemented during phase 2, 3, etc of the current pandemic.

Actually: the previous paragraph summarizes quite well the real title that many of those commissions should be called.

I am not being cynical- it is "Realpolitik": over the last couple of weeks, the jokes about the number of Commissions set up at the national and local levels are reaching a Soviet-style level of jokes.

We will soon need a meta-commission, i.e. a commission of commissions about commissions.

Few days ago, I saw a banner shown during a protest from health personnel that said (literally) that locally there are more members of the various commissions than newly confirmed infected by COVID-19 (I wish it were really so).

Personally, I am just preparing for potential new activities as it seems that the only activities that I could be allowed to do here are actually either unpaid or in support of somebody else officially appointed to do what I used to do.

Therefore, I am invisible enough to avoid joining the fray.

Also because, as you know (if you followed my online publishing in various formats since 2008, or were a business reader of my e-zine on change 2003-2005), most of what I shared in the past about change could actually be "recycled" (as some did) now.

So, I will jump to my main point for this short article.

Smart: spending, investment, working

I shared on Linkedin a newspaper article about what in Italy is called "smart-working" (i.e. working from home).

The article (see link and post here) states that 1 out of 3 (office worker) will keep working from home.

Well, read what I wrote in the past about Italy and the local approach to digital transformation, business 4.0, and all the "innovation" paraphernalia.

The key point is: instantaneously transferring everybody home showed shortcomings on at least three levels.

On the infrastructure side, as we are still way behind in e.g. FTTH (bringing broadband in each home by extending fiber to buildings, not just exchanges, as approximately 30% of the Italian population still lives outside main urban areas).

On the "enabling technology" side, actually its lack thereof, as shown by the sudden increase in PCs purchases, so much that some talked of a potential shortage, due to the contraction of production in Asia and ensuing disruption of supply chains.

And, last but not least, on the "human capital" side, as many processes, also in offices, are still structured assuming "eyesight presence", i.e. supervising by looking.

I am talking about business: now, think about schools and pupils that are supposed to keep being "virtual students" for a while, with some schools reporting missing 25% or more of them, a country where over 20% is over 60 suddenly having to do everything remotely from home, or a cash-based economy suddenly jumping onto plastic money, just to name few side-effects.

As I wrote often in the past, and as I learned first in political activities in the early 1980s, then in software development in mainframe environments, and from the late 1980s in business models for decision supports, no matter how "smart" are your ideas, it is their implementation that turns them into a success or a failure.

And implementation is rarely "greenfield", as e.g. was for the e-government in Estonia (disclosure: 2015-2018 was "e-resident").

More often, both in the private and public sector, you have to cope with layering of regulations, practices, "our way of doing things", etc that span centuries (in Italy and China, millennia).

In Italy, as I wrote often, we have our past to look at (obviously Roman Empire and Renaissance), but we lack the stomach for complexity and "lifecycle of initiatives".

In politics and business, we are way too often focused on a Yuppie-style "low-hanging fruit" approach.

And this is of course due also to our cultural left-over from well before the Renaissance, our "tribal" attitude to society.

As shown by many Italians who lived and worked abroad, we aren't "genetically incapable" of living and working in a structured manner, when needed.

It is simply that, in a country where everything is bartering and negotiable, bartering between tribes, and negotiable to keep the balance of power between tribes, or rearrange if and when of interest, nobody is really willing to be exposed to long-term investments that could depend on such a volatile balance to be successful.

One of the obvious side-effects is that, if you compare with other more "ordinary" countries, in Italy the debt is predominantly a State (or local authorities, to a more limited extent) affair, while assets are private.

This is just a first article on the theme, so I would like to start with the consideration that I posted yesterday and today in the morning on Linkedin.

The latest first (I am sharing the Facebok version as it does not require login): an Italian newspaper this morning complained that FIAT/FCA is considering accessing the facilities provided by the Government to support Phase 2 of the COVID-19 crisis, i.e.subsidized credits (and potentially grants) for companies to open again.

The reason of the complaint? The mother company is not Italian anymore.

Frankly, it is a quixotical complaint: recently I heard from our own "pocketsized multinationals" that, for their operations abroad, received COVID-19 funding e.g. in USA and Germany.

As it should be: the point is restarting sustainable economic activities that support local jobs, not where their headquarters are- that is a silly and outdates concept of business realities.

And it is not that I am positive about recent repeated initiatives from FCA during the COVID-19 crisis, while many others were thinking too short-term, just because since 1986 and until 2018, I had repeated projects with companies within the FIAT or FCA group.

Also in business, I like to look at facts: it applies to any company.

The point isn't accessing incentives if available: to explore, and, if useful and applicable, ask for those incentives should be the duty of any CEO and CFO.

If anything, my criticism of Italian companies is usually the opposite: I heard way too often questions such as "what can we do that is covered by incentives?".

What matters, is the design of incentives.

Incentives for Phase 2: an opportunity or a cost?

Personally, I think that (and I am not the only one) too many left, centre, right have a political interest in currying the favors of current potential voters, but in so doing are not using this as an opportunity to at last restructure the Italian economy, investing in the future while transitioning from the past.

Instead, too many are supporting a grants-based economy, both for individuals and companies, subsidizing businesses that already recently were nicknamed "zombie", i.e. surviving just thanks to low interest rates.

A grants-based economy focused on the short-term, whose long-term cost will fall on future generations.

I do understand the personal attachment of most of our small family-owned businesses to continue their own business- and this is were "leading the transition" would matter.

Italy is already under the strain of a debt that affects the freedom of any government to set up and deliver initiatives.

Adding more debt that doesn't build a sustainable future is useful maybe to win the next election, but what then?

And not too distant in the future: just looking less than a decade into the future, choosing now the balance between future, past, and transition will impact also on the political career of most current politicians.

It is curious that usually the accusation of "spending without restraints" was levelled on the left, while now those advocating "spending without limits to restart" are spread across the political spectrum.

As I wrote often in the past, I am bipartisan: hence, I have no qualms about helping companies that can restart a sustainable activity, to help them offset the costs involved in this crisis.

But I have plenty of qualms about "coronadressing" failing businesses that simply struggled to survive in the old economy, and would absorb resources that would be needed.

I will return to this point later, but let's now instead look at the other them, "smart working".

Shifting 1/3 (I think that the figure is wrong- more about this later) of the workforce to work remotely implies restructuring processing and "chain of command"- better, leadership styles, and, as well, flattening organizational structures.

Incidentally: why do I consider that figure wrong?

Because sounds a lot a "media del pollo", as we call it in Italy.

Somebody eats no chicken, somebody eats four, so "on average" is akin to stating that "the average income per person in Italy is X".

So, what would be the impact?

In this case, I will spare you the effort to read (or re-read) my past books and articles.

Quite simply, you cannot lift one person out of a process under the ordinary conditions, and have it still working: that is just playing lip service to "innovation".

Instead, consider that what worked now was an emergency, productivity expectations were relative, but at least many "discovered" how many of their processes, meetings, calls, paper/e-mail shuffling was just façade, not productive work.

Albeit, during this emergency, most members of a "process team" where equally working from home- hence, the "ordinary" process and "chain-of-command" structure (as well as interfaces and exchanges between them) were all "flattened".

Hence, more than a "1 out of 3" quota, should be considered which processes and which interfaces between processes could be transferred outside.

Human and technical interfaces: in our times, most people think about technology first, people last- albeit, in order to work, any process requires a mix of both.

There will be a temptation to instantly replicate what was done now: but, again, it was an emergency, when many things were tolerated (probably both by employees and companies).

So, automating what apparently wasn't "needless human interaction" based upon the "lockdown" experience would be short-sighted.

At the same time, replicating what was made workable now could create issues downstrean- in an emergency situation, you can cut corners and strain resources, but that has to be for a limited amount of time and justified motives.

If you were to convert it into the "new normal", you would actually start seeing organizations falling apart, productivity go down the train, and... spending more time implementing a "Big Brother"-esque approach to business life than actually carrying out business.

And this, exactly at a time when being able to compete as a business would require more involvement of all those involved: a kind of "converting the control-freak Leviathan in Hobbes into a swarm-like organizational structure".

Something that would be nothing really extraordinary (except for the different kind of "management roles" required): simply, each part of the organizational supply chain (suppliers, employees, customers) would be an "antenna on reality".

You actually already started to use it since at least a decade, in your equipment, e.g. your car collecting (and maybe even broadcasting) information on its use.

The critical point is transferring that attitude toward your "human capital"- and that requires proactive collaboration, not one controller every two employees.

In a twisted way, it is a scenario actually closer to what I saw since the late 1980s in business: outsourcing a process while retaining control and "knowledge continuity" isn't for the faint of heart.

Including internal outsourcing: from management to employees- which isn't just "delegation", it is something more.

If curious to see more details, but in a more structured way than across articles, have a look e.g. at BFM2013 or SYNSPEC, or even BSN2013- old books that I published in 2013 or slightly later, but still useful for the "cultural and organizational change" concepts in business.

Short storytelling on a possible future/present

For the time being, I am more interested in thinking about impacts, so I will summarize a bit of ideas that I already partially shared in the past, assuming that this crisis lasts at least until the end of 2020.

Just for the sake of boredom, I will simply share few "short stories" about that could happen in automotive, banking, retail, and the evolution of urbanization.

As I said, I worked on projects for automotive customers for over 30 years, mainly on the IT side, and, on the IT side, mainly on the management reporting (and related) side.

Anyway, when you see a business from that side, you learn to see it not as a set of products, events, parts, etc- but as a lifecycle.

Now, many are stating that, due to current COVID-19 restrictions, the automotive industry lost over 90% of its sales in Italy in 2020 vs. 2019.

And, due to the restrictions for phase 2, many are celebrating the demise of the "car sharing" business, and are questioning public transport.

This might be true in countries that never developed public trasport, but I worked across Europe in various countries, and saw first-hand (as I do not drive) the life of commuters.

In Italy, we aren't that far away from the most urbanized EU Member States (population-wise, we are at 70% and some, others exceed 80%).

Remove public transport in, say, Turin, Milan, Florence, Rome, Naples, and life would stop (at least during working hours).

So, it might well be that the car market will have a "bump", but our consumption model has changed a while ago.

As I wrote last year, many in their 20s and 30s have a driving license, but do not own a car- or own a car just to park it (e.g. a used car), and use car sharing.

Well before COVID-19, I shared some ideas about the "share economy" which, for cars, included thinking about a different design to enable robot-driven sanitization of vehicles between uses, e.g. by applying a removable "film" inside the vehicle, removed, disposed, and replaced after each use.

Do not accept a "coronadressing" (to obtain incentives) of this basic need that was unfulfilled before: it was something that was eventually to become a need.

Currently, at least in Italy, we can just hope that the traditionally nice May weather will enable more to discover individual mobility vehicles such as electric skateboards (and both the Government and local authorities are either considering or announced financial incentives), or, who knows, something as those "eggs" shown in an MIT study done few decades after the 1990s Womack study, "Reinventing the Automobile: Personal Urban Mobility for the 21st Century" (link to my review released on 2018-05-22).

Short-term, probably there will be a limited lifting of current limitations to car use, also because on public transport de facto the limitations imply more than 50% of the avaiable places (e.g. in Italy only seated passengers are formally allowed for now, albeit there is no real control).

If coupled with increased "smart working", working hours spread across the day, and other work routine changes...

Well, if taxis are being revamped, but with the enforcement of stricter safety measures, this will imply putting out of business Uber and others, as, from my reading e.g. of current Italian COVID-19 government degrees, they are unable to comply with what is required.

This applies to others within the sharing economy, of course, but more about this later.

Back to the car industry: if the current crisis last longer than few months (probably it will), we will get back to old approaches for a while, but, if anything, this will be an incentive to create new forms, shapes, approaches to shareable vehicles, not a a motivation to think to a 1970s model of ownership.

The latter, might appeal older people (including those, like me, in their 50s), but for many (myself included), the point is thinking about what would be needed to keep developing a more efficient allocation of resources.

And efficient allocation of resources is another element that will impact also on another industry whose organization and structure studied and worked in for a while, banking (first project, 1987).

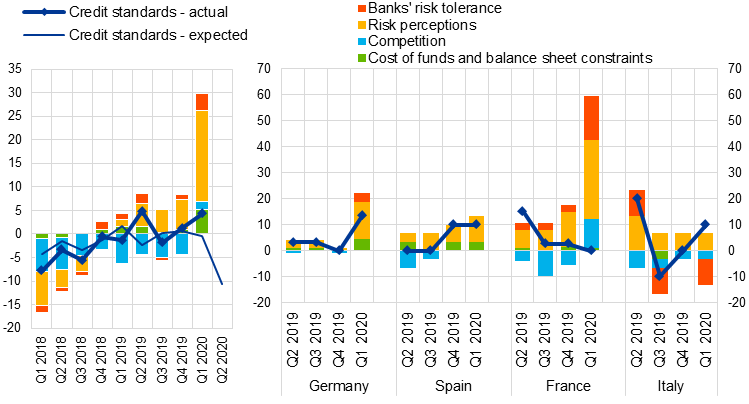

Right before the crisis officially started with the WHO declaration of the pandemic crisis, as recently remembered by the ECB (in a press release on April 28 2020, "April 2020 euro area bank lending survey"): "[in the first quarter of 2020] For loans to households, the net tightening was somewhat stronger than for firms (a net percentage of 9% for loans to households for house purchase and of 10% for consumer credit and other lending to households). Banks referred to the deterioration of the general economic outlook, increased credit risk of borrowers and a lower risk tolerance as relevant factors for the tightening of their credit standards for loans to firms and households."

Then continues "For the second quarter of 2020, banks expect credit standards to ease considerably for firms, probably on account of the support measures introduced by governments. At the same time, the dispersion in replies highlights the high uncertainty surrounding the likely impact of the coronavirus (COVID-19) pandemic and the different views of banks on the impact on bank lending conditions. By contrast, the net tightening of credit standards on loans to households is expected to continue in the second quarter of 2020."

Furthermore, "A strongly negative net balance for demand for housing loans and consumer credit is expected by banks in the second quarter of 2020."

In visual terms, as shown in this chart (from the same Press Release) with the title "Changes in credit standards for loans or credit lines to enterprises and contributing factors":

Look specifically at the risk tolerance and competition.

Now, I will follow just one thread within the banking industry: organizational structure and local presence.

So far, banks apparently, beside tightening credit to households and generally consumer credit, something that will lower needs of "branch level access", went in different directions.

Just to stay in Italy: a major bank months ago announced that it was closing few hundred more branches, while a smaller bank trying to expand its market quota tried to differentiate itself by its presence within territories- opening branches.

Abroad, a major bank in UK instead announced the demise of mega-buildings where to concentrate specialist teams, something that, risk-wise, was actually suggested e.g. after 9/11, and proposing instead to spread them around.

As I posted on Linkedin few days ago, probably a side-effect of the current wave of forced remote working and current trends could produce some significant changes.

Now, if you were to close branches, who would take over that real estate?

Better then to reuse it for something else- such as what the UK bank proposed.

Value added: if, in the future, there will be a need to routinely restructure also the physical presence, having a building capable of hosting, say, thousands, and with just a quarter of the occupancy would be a waste and a bad sign.

After getting those who can work remotely work remotely, it would become easier to become more flexible: also the banking business model will need to adapt to new forms of competition.

While for months and maybe even years there will be a rethiking of the "uberization" within the physical economy (i.e. making demand and offer meet by temporarily allocating efficiently unused assets belonging to others, not as a market, but as a "virtual organization"), it is to be expected an expansion within services such as finance, insurance, up to asset management.

If you think about it, frankly, it is really nothing that much innovative: it is a XXI version of the Lloyds market.

Therefore, probably could make more sense to retain smaller branches as "containers" to be used for whatever use is needed, e.g. to enable the use of the real asset of banks: the aggregated wealth of cross-disciplinary knowledge.

As an example, why not to imagine a multi-disciplinary product team allocated to a branch temporarily for a mission, while still being linked to its own "domain" line?

It would be intra-company uberization, a demand-and-offer, made possible by the removal of compulsory physical continuity.

As a Japanese classmate one summer at LSE told me once, he was there as his Japanese financial company wanted him to work on a new activity that they were setting up in UK (it was early 1990s).

Part of the process, as his organization was structured about specialties, had been to spread his portfolio across his colleagues- so, no way back.

Moreover, that move "suggested", if the new initiative were to be folded, implied that he would lose rank and seniority, if he were to return, so he knew that that was a one way road.

He had received unusually good terms for this move for him and his family, compared with what I had been told by an American colleague who had worked with other Japanese large companies years before, but still it was a one-way road.

Now, in the XXI century, if you remove that "structural rigidity", you need to have also a completely different approach to talent management (and career management), but in some cases it is still true that if you aren't were "the grapevine" feeds careers, you might be the biggest in house expert, but your talent will go unnoticed.

If, instead, you spread teams, you need to design a "competence market and scoreboard", so that any part of the organization can access those talents, negotiate uses, and "barter" (if that is your approach).

Well, this post isn't about banking, so I will let you derive other potential consequences, the ups and downs of the options listed above, etc...

... but I will stay in retail.

Short-term, at least in countries where small- and medium-sized shops are common (most of Europe), it is actually a nightmare, let's just think about food and clothing.

I do know you, but when shopping I was used to try clothing, shoes, headgear...

Well, some of my Linkedin connections were into the "virtual" side of that, and, probably, will find new demand.

Would you, for example, purchase now from the rack something that isn't packaged, and maybe has been touched or tried by others? Doubtful.

I remember long ago reading an article about tests done on clothing, to identify all the "impacts": it was akin to those pictures showing hotel room density of bacteria etc.

So, it used to be advisable to wash whatever you purchased, before using it.

Now, considering how long COVID-19 can stick on surfaces if there are the appropriate conditions of light, humidity, etc, it seems that clothing is a good breeding ground- but I will let to other to check.

Maybe on this side we will have more "virtual shopping", extended up to an Ikea style, but with "virtual try-on" in shop, then leaving the shop with your own "unit" of pre-packaged, never tried, never used of that specific item.

And, of course, this could make also possible an expansion of e-commerce, and, why not, more smaller yet more technological shops.

As for food, Amazon and others already tried the "humanless cornershop" approach.

As I said to others and shared repeatedly online, most small cafés and bars in Italy would cease to be economically viable, if they were to, say, ensure 2mt between customers, and follow other measures.

Still, most could (and since yesterday it seems that they are) open as a kind of "take away".

I saw a picture of a tiny café, one of those where half a dozen people seemed a crowd, in the past, and now would be unable to have just one customer sitting while still be in full compliance with COVID-19 measures.

So... the owner simply put a table across the door, and turned into a kind of "walk past café": call before asking for what you want, and then pass and pick from the table what you ordered.

For family-owned cafés, this could be a solution.

But those who had staff, will probably have to release most of the staff.

Anyway, despite what some politicians and journalistw say, both hotels and restaurants or cafés routinely used staff "on demand" (and often also without proper employment contract, including in towns such as Turin, Milan, Rome).

So, try to pile up on COVID-19 some structural weaknesses that pre-dated the current crisis is, again, another case of "coronadressing".

Many would not have been economically viable in the first place if they had had in the past all their staff on payroll: so, it is at best quixotic to use now as "human shields" staff that they never officially had, in order to obtain benefits.

This is not a general rule, of course: if you had, say, 20 tables barely 50cm apart one from the other, 4x5, assuming a table of 1sqm, and you have to keep now them at least 1mt apart plus add transparent dividing walls, it means probably having now just 3x3 tables.

So, also if you had before full-time, "registered" employees, now you would need less.

I will make a (fake) computation of the "capacity planning) for a restaurant with no outdoor facility, and 20 tables, assuming, for simplicity, a restaurant with a single rotation per meal (i.e. only one party would use that table).

Reason: assume that it is a place where people go and stay (business lunch, dinner), probably geared toward the higher end of the market.

Also, this removes another complication: if you have to comply with COVID-19 measures, you have to ensure not just spatial, but also temporal separation, i.e. if you have two rotations, or three, you have to ensure that people enter one way, go out the other way, and never cross, while you also have time to sanitize between rotations.

So, let's assume just one rotation (would expect 2-3 in ordinary times at lunch, with a 2 hours opening, and 3-4 in the evening, with a 4 hours opening).

Moreover, if your restaurant was geared for, say, at least 30% occupancy rate on average, but used to full-occupancy at lunch five days a week, and at dinner also on Friday, Saturday, Sunday, let's see the difference.

Before: 4 nights x 20 x 30% + 5 days at lunch x 20 x 100% + 3 nights x 20 x 100% = 24 + 100 + 60 = 184 tables; assuming an average of two people per table, 368 meals.

The "average 30%" means: you have 20 tables, available at lunch 5 days, plus 7 days at night, i.e. 20 x 5 + 20 x 7 = 240, on an average of two people per table, means 480 meals

You 30% would be 144.

Now: 4 nights x 9 x 30% + 5 days at lunch x 9 x 100% + 3 nights x 9 x 100% = (rounding up) 11 + 45 + 27 = 83 tables; assuming maximum two people (impossible to comply with COVID-19 measures and have more than 2 people seating at a 1sqm table): 166.

So, it would still seem profitable, but, as many commentators forget, you have to factor in:

- the costs to update the structure

- the human element, i.e. fear

- last but not least: would your supply chain increase prices if you move from purchasing supplies for 368 meals, to 166?

Also if you were still in the black, you would move from being a highly successful restaurant (100% five times at lunch and three times at dinner was what enabled being closed at lunch on Saturday and Sunday), to one that barely survives, or would quickly sink into the red.

Moreover, there would be zilch space for investments, renovation, etc.

Restaurants and cafés, in many forms and shapes, are ubiquitous in Italy, and part of the local social life.

If not a restaurant, visiting few times a week a café is an Italian routine that nobody (myself included) escapes from.

It is not just about consumption- it is about socialization.

The Italian version of urbanization isn't really akin to the technocratic approach suggested by some: yes, we have office districts, but they are used also in the evening ("apericena", restaurants, etc).

A side-effect of the COVID-19 crisis was shown on March 8th, the night before the first batch of nation-wide measures was to be enforced, when many returned from the North to the South, and was seen again earlier this week, as soon as, on May 4th, there was a partial re-opening of the possibility of returning home (we still cannot leave the region where we are, unless for business, health, or to return home).

As many activities still will not resume working soon, and anyway schools will be probably closed until September, many more will choose to return elsewhere (on May 4th, reportedly all the buses and all the flights and all the trains were fully booked).

The closing down since early March resulted in some changes also in retail, but temporary changes, as for few weeks you could not leave the town where you were.

So, supply chains had to be re-routed, and small village shops suddenly had a flow of customers they weren't used to.

Some adapted, and will retain customers, others had a "peak of revenue", but short-lived.

One of the obvious side-effects will be on AirBnB and its siblings: in major Italian towns, as I saw in Turin, frankly this kind of "impromptu hotels" (as de facto many rented just to... AirBnB), the scourge of continuous trolley people and their "who cares" attitude to temporary occupancy of residential areas was becoming a nuisance.

Will they be able to comply with COVID-19 measures? Doubtful- but in future cases, if I were to live again in towns such as Turin and Milan, one of the criteria for choosing an apartment would be "no bed and breakfast, no AirBnB".

There are actually some other impacts already being discussed on urbanization, i.e. the adoption of a French-style relocation of offices outside residential areas, to avoid the nightmare of ensuring separation etc.

Not just for the companies: imagine if you were an employer whose offices are within a residential building.

Now, you can take all the measures you want to ensure compliance.

But you need just one ill-advised residential inhoccupant of your building who is careless and infects e.g. shared spaces.

Ending up with a nightmare if your employees or your suppliers' or customers' employees then get sick and, eventually, the "urcause" is discovered to be... somebody who complained a lot about the COVID-19 measures and publicly stated "I do not care, it is all a conspiracy"...

Also mega-office buildings within residential areas could be troublesome, due to the need to ensure spatial and temporal separation.

The current partial reopening, with bleak perspectives about what could happen between now and probably Spring 2021, will push more to return where they came from.

Just to consider Piedmont, in the 1950s and 1960s the automotive industry generated an internal migration from Southern Italy and Veneto.

So, many will probably return home- often retirees, but also university students, and various universities already announced that they will keep being "virtual" well into 2020, and probably until Spring 2021.

Hence, more people who were temporarily in Northern Italy will relocate elsewhere, reducing the use of local facilities, but increasing demand for services in Southern Italy.

No matter how short, this could push for more harmonization across the country.

The current crisis, with everybody having to work and attend schools remotely (or not at all) resulted in renewed demands to complete the rolling out of broadband, as well as to reduce the digital divide across the country and across generations.

Recently, the Italian Presidente del Consiglio dei Ministri, Mr. Conte, shared his idea that Internet should become a constitutional right.

The same approach adopted years ago by some other countries, but could be one of the benefits of this crisis.

Another benefit could be forcing our small companies, an element both of flexibility and weakness of the Italian economy, to embrace co-opetition.

Do you remember the example I made about a fictional restaurant?

Well, imagine a small company with equally cramped production facilities.

Just the mere restructuring of workflows and production lines to ensure physical and temporal separation would make many not viable.

In some cases, they might have the space needed to restructure and introduce measures, but they will lack the staff to ensure compliance and procure a continuous stream of supplies of individual protection devices (masks, gloves, etc).

Pooling resources, something I already discussed in previous posts, might be the alternative to keep being closed.

Also, co-opetion, joining forces with your erstwhile competitor, might imply a rethinking of organizational structures and management approaches- something that is sorely needed.

As I shared long ago, a large German company had to pay a penalty for failing to deliver, and the failure was due to the delays generated by a much smaller Italian supplier.

Did they replace the supplier? No- the German company said that liked their products and expertise, so purchased the company and provided management.

As I wrote today on Linkedin, I do not think that having the State turn into an investor and provide governance to small and medium companies is a solution.

The State over the last couple of decades as been unable to provide oversight and governance even on privatized critical national infrastructure, where do they plan to find the people needed?

It risks turning into the usual "poltronificio" that in a previous political season gave us "partecipate" and plenty of non-profit "foundations", i.e. companies belonging to local authorities but formally private, used often as a sunset boulevard for politicians who gailed to get re-elected, or weren't anymore the right person for the right time.

As I wrote in the past, I think that it would be more appropriate for industrialists' associations and trades unions to support smaller companies in their organizational renovation efforts.

For at least three reasons:

1. both small companies and their representives and counterparts need to develop their own organizational culture

2. currently, only few Italian large companies (private, PLCs, and State-owned) have the organizational culture needed to compete abroad

3. in the future, we will need more organizational cooperation between all the parties involved (yes, "stakeholders", but I would like to avoid that term now).

Also, at last, recently large Italian companies here and there announced to be open to the idea of co-opting trades unions, German style, and this would require a massive creation and development of talent and careers within trades unions, whose top management way too often sounds as if lifted from the 1970s.

Conclusions: it is safe?

I concur with what I recently heard (remotely) in a conference: over the last couple of decades, Italy missed a train- in my view, since right after the Y2K craze, we started diverging, the Euro impact was a side-effect, not a cause, also if, now as then, I think that we entered with too high an exchange rate the precursor of the Euro.

It wasn't a bad or short-sighted political choice, or a sell-out, as some claim: simply, most would like to ignore or forget our real bargaining power back then...

... as they would like to ignore it now.

What I heard at that conference was funny, and I agree with the main point: we missed a train, while other countries kept moving; now, everybody stopped- so, if we play it well, we might restart as the other do.

I have obviously some differences about the "cure" proposed: I still think that streamlining bureaucracy is but an element, we need a stronger assessment of our infrastructural and cultural business/social weaknesses, something that I shared here.

Currently too many are asking to invest future generations' revenue to support current floating of businesses that had no resilience.

Also, it is true that we are all on the start line now, but we are starting from different level of strengths, exposed even more clearly by the management of the current crisis by our political, business, and social elites.

Too many looking short-term, too many quarreling to score points, too few considering the long-term impact: survival of the fittest isn't a solution, but usually is the one proposed by those who assume to be the fittest...

I disagree: pushing every resources to kickstart now while mortgaging the future, and this just to keep going as if nothing had happened isn't simply short-sighted, is self-defeatism.

Because countries that re-started from a stronger position will be better able to leverage and add resources when opportunities will be available.

It isn't just debt and bureaucracy that are a burden, a true ballast on the potential of Italy to adapt and adopt what is needed to move ahead of the pack- it is being oblivious to the need of a reconsideration of our role.

Is it safe? Well, we do not know yet- both if we are talking about COVID-19 and the economic and social ability to cope with the current crisis.

Shortcuts toward a technocratic weakening of democracy will not generate the kind of social conscience needed to benefit from digital transformation and leap-frogging ahead of our national infrastructural backwardness.

There was a press release from the ECB, released on April 30th, whose title sounded a boring "technical" element.

But the closing statement was chilling, a sign of the open-ended crisis we are in, and whose side-effects, and exposure of structural weaknesses, will take probably years to study and repair: "The Governing Council is fully prepared to increase the size of the PEPP and adjust its composition, by as much as necessary and for as long as needed."

What is the PEPP? The Pandemic Emergency Purchase Programme- you can read on the ECB website ten items released between March 18th and May 1st.

Many are talking about "reshoring", usually coupled with "reshoring incentives".

Fine- but consider that, unless you also take this opportunity where most businesses are anyway closed to dramatically restructure supply chains and production lines, including with an expansion of automation, any money that were to be dumped into that bonfire would warm for a while, but probably not even until the end of the Summer.

Then, we would be in for a cold business winter.

There is time- but time for thinking and rolling up sleeves, before just simply tossing around cash to sustain what basically brought us where we are.

Do you want to use this opportunity to relaunch the country?

Well, then it is the right time to invest- on physical and human capital.

Also if this were to cost some political capital, short-term.

Stay tuned...